Behavioral banking or the hyper-personalization of banking services is relatively new and is only being practiced by a handful of banks globally. However, those who’ve taken this approach are quickly gaining traction and differentiating themselves for competitive advantage.

Dr. Christoph Markert, the Head of Architecture for SAP Fioneer in Asia Pacific, takes a deep dive into behavioral banking, including:

What is behavioral banking?

The benefits of behavioral banking for both the bank and its customers

Principles and architectural infrastructure needed to deliver behavioral banking

What is hyper-personalization?

“Some of the most successful companies on the planet are built on the same fundamental premise; an API-driven platform, through which they deliver value-added services to customers by using insights derived from vast amounts of data.”

Think Facebook, Apple, Amazon, Netflix, and Google (or ‘FAANG’ as they are affectionately known).

And we’ve all experienced it. They have different approaches to the behavioral science underlying the personalization they deploy — Facebook uses a ‘magnet’ based approach, Google has its ‘toolbox’ that simply accelerates inter-connectivity and Amazon with its ‘matchmaker’ approach. You know the drill — Amazon says “Christoph, 90% of the users who bought this laptop also bought this wireless headset” and you say “Fantastic! I’ll take 10!”

Not data, but insights

But what these companies have in common is that they are delivering value to their customers, whilst differentiating themselves in the marketplace. Amazon Prime for example creates this value and differentiation simultaneously by turning the movie preferences of customers not only into streaming suggestions but into inspiration for new content.

To achieve this, data is obviously key. But raw data itself can be difficult to understand and process.

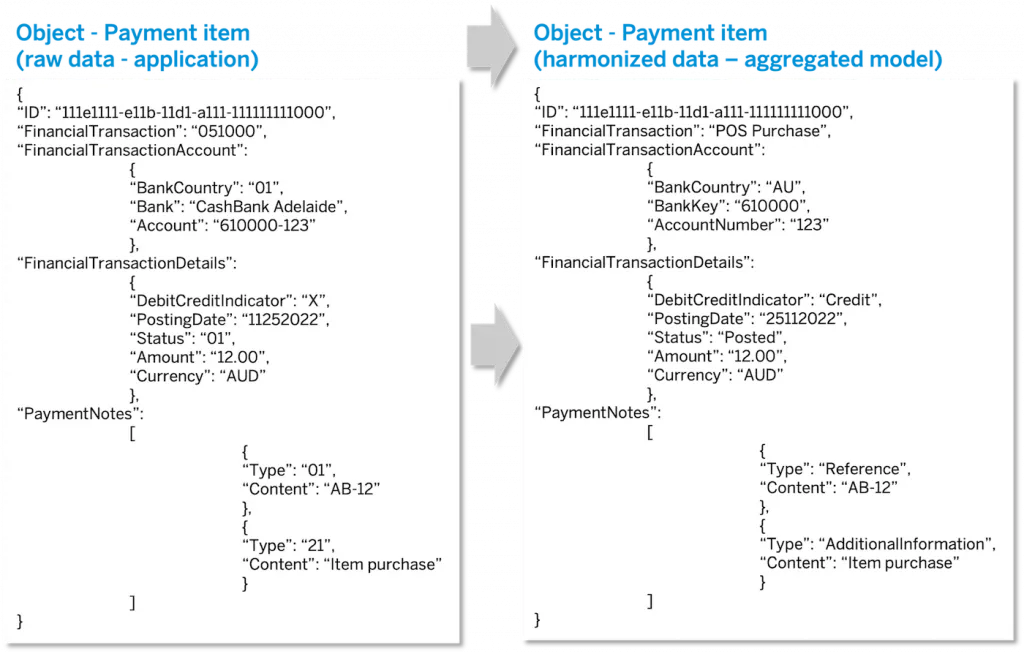

First, your data needs to be curated into a common format and structure detached from the underlying internal data format of an application. An example of how this could look for a financial transaction is shown below:

Behavioral banking – data models

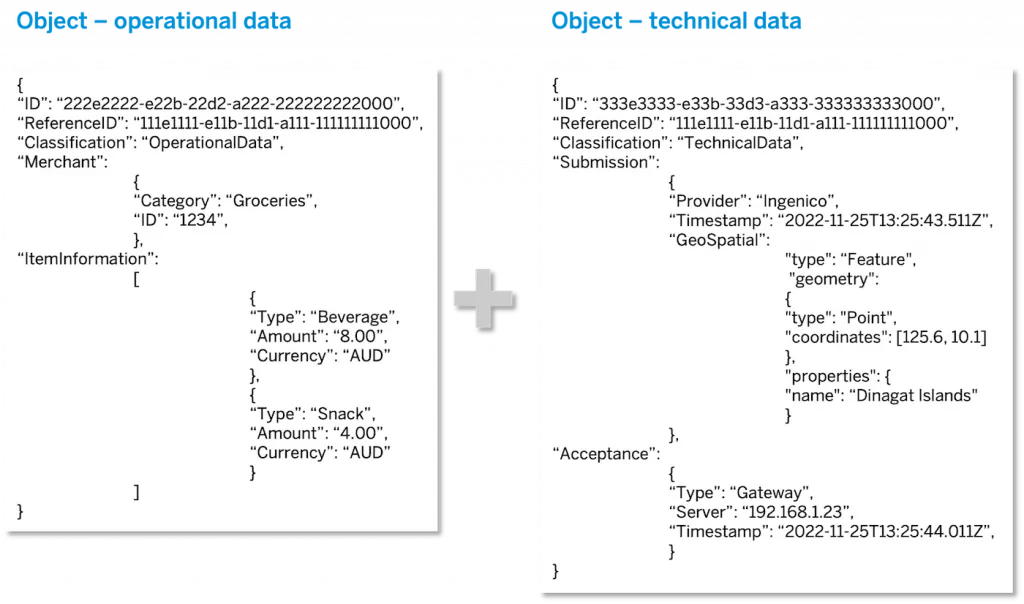

Secondly, you need to enrich data with value-added information via meta data and virtualize it to make it easily accessible for consumers – combining operational data about a transaction for example with technical data, like location.

Behavioral banking – metadata enrichment

Behavioral science: the origin of hyper-personalization

When we turn on Netflix, we expect and accept that the service will make recommendations based on our prior streaming behavior, or that of our cohort. Behavioral science is in turn influenced by other disciplines, like social science, psychology, and anthropology. Indeed, culture can be a significant influence, and as a part of that, generation. If you go to Mcdonald’s, whether you choose to go to the manned counter order via the self-service facility, or the app, is largely driven by your age. The same applies to banks: how many people in their 20s do you see in a bank branch these days (apart from the tellers)?

“Welcome to a bank that doesn’t just store your money but changes your relationship with it.” — Discovery Bank

What is behavioral banking?

Behavioral banking specifically is the use of insights from data to improve the financial well-being of customers by offering them tailored products and services.

And how is this done?

Largely through incentives. Customers can be rewarded for spending less. Or reaching savings goals. Or paying off their loans earlier.

Prompts to improve financial fitness have become as acceptable as those for physical fitness in developed countries. Historically, this was largely the remit of standalone PFM (personal financial management) apps but increasingly banks are taking PFM on and raising it to the next level. As Falk Rieke, the Global Vice President and Global IBU Head for Banking at SAP said in 2020, banks are ‘changing the game’ on financial literacy.

Incentivizing better financial behavior with dynamic financial products

The most common rewards are dynamic interest rates. If a customer reaches a savings goal, this can trigger their savings interest rate to increase, or the rate on their loan or credit card to decrease. As they progress, they unlock new rates, and this can lead them to pay off loans earlier, for example.

But why would a bank want to do that? If the lifetime of a loan is reduced, surely it would earn less interest?

What are the benefits to banks for behavioral banking?

The benefits to the banks and customers can be considerable. As Klaus Wertenbroch, Professor of Marketing and Management at INSEAD says:

“The benefits range from improving customer relationships with a bank’s brand by building feelings of trust, fairness and dignity to more tangible benefits such as improved financial well-being for the bank’s customers.” — Klaus Wertenbroch, Professor of Management, INSEAD

But it’s also good for the bank’s bottom line. What they lose in interest can be offset by increased cost savings or returns elsewhere. Discovery Bank reports:

Customers with higher financial awareness and literacy are less likely to go into arrears on loans. Chasing arrears is not a bank’s core business and is a costly distraction.

Whilst this might mean paying out more interest, it also means a larger source of cheap funding for lending operations, so pretty key for a bank’s main business model.

And as KPMG points out, providing customers with financial wellness opportunities drives engagement and

“Studies show that engaged customers bring 37 percent more annual revenue to banks” — KPMG

A behavioral bank provides a fully digital, hyper-personalized banking experience

Behavioral banking is directed at an audience that is currently middle-aged or younger (who are banking digitally).

As such, it’s mobile-led (from onboarding to transaction) and omnichannel, as this generation often hops between mobile, tablet, and desktop. Active rewards go hand in hand with gamification. The motivation can go beyond dynamic interest rates to external benefits, such as frequent flyer points delivered by a partner, or even basing interest rates on the progression of a customer’s favorite team in the world cup, as with Postbank in Germany (please note we are not endorsing this!). As part of opening up to these benefits, integration to a broad partner ecosystem via APIs is key.

How is behavioral banking enabled?

1. Start with a simple product

It’s best not to start with a complex loan but something simple like a transactional or savings account with a card – this helps you get to MVP faster.

2. Attach dynamic interest rates

Dynamic interest rates – on a savings or a loan account – are a fundamental reward component.

3. Push the information back into the core banking system

What we call at SAP Fioneer the ‘financial conditions’ are in this context highly individualized and multidimensional – taking into consideration the customer’s data including environment, interest rates, fees, existing product portfolio and so forth.

4. Deliver it through a highly intuitive app

The quality of the UX (user experience) is critical to the user understanding and successfully interacting with the behavioral bank. Responsiveness, consistency, familiarity and intuitiveness are key.

Banks need a highly scalable, reliable, rock-solid foundation to run on. If your account management or payments system fails, this could not only play havoc with a bank’s operations but could lead to a disastrous data-driven customer experience.

Agility

A consistent architecture enables the product team to design and test new products, services, and related features rapidly: fail fast (but learn from your mistakes). Ultimately, the end-to-end architecture needs to support the creativity of the business to build market differentiation for the bank.

Speed

In a hyperconnected world, speed is a pivotal element to offer personalized services to customers. The pace at which information is consumed, analyzed, harmonized, and processed can make all the difference to a cross-/up-sell opportunity or a potential new revenue stream. A brief plug at this point for the SAP S4/HANA in-memory database which we at SAP Fioneer use as the underlying database platform because it means information and services can be accessed significantly faster than they would be with conventional database architectures.

APIs

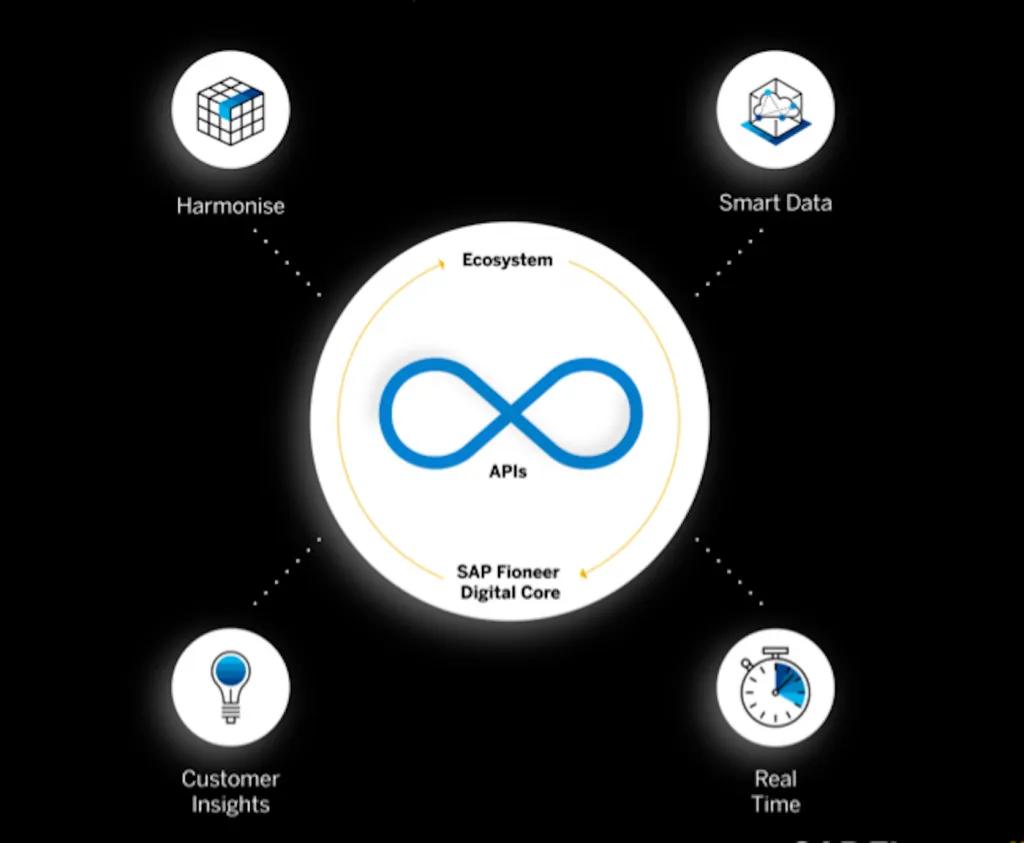

Of course, behavioral banking relies on APIs. These interfaces don’t just enable banks to execute daily business operations that create and update content but also provide the data-derived insights they need to understand a customer holistically. Standardized APIs and events provide a harmonized way to not only share information in real-time, but to integrate applications from a broad partner ecosystem in a way that’s flexible yet low-cost. However, digitally driven banks don’t stop with harmonized APIs. Smart information models allow banks to tag additional, value-added information to the data itself. These models help us understand the purpose of some particular data points more consistently and easily. Subsequently, these insights are pushed back into a digital core banking application via APIs to trigger the personalized experience. And so it goes in an elegant circle.

SAP core banking – openCore ecosystem using APIs

Get ready for the win-win

However, the true elegance of behavioral banking is that it creates benefits for both customers and banks. Tailoring services and products help improve customers’ financial literacy and outcomes, whilst reducing risk for banks and increasing loyalty. It’s time for a new personal service.