Subledger vs. general ledger: Why financial institutions need both

7-minute read

Published on: 19 March 2026

The general ledger tells financial institutions what happened, but not why they happen.

With the general ledger, an institution can see interest income increased by €3.2 million or that a provision was raised. But it can’t see that the interest change was driven by rate, volume and behavioral effects or that risk migration and updated expected-loss assumptions caused the provision.

Only a subledger provides the underlying reasons, showing which events, assumptions, risk movements or valuation changes produced those outcomes.

This difference matters because financial institutions increasingly need not just historical reporting, but forward-looking, risk-integrated insight to guide strategic decision making. Deloitte found 72% of banks have defined a data-quality risk appetite, but only 17% have operationalized it—exactly the kind of control gap that detailed, traceable subledger data helps close.

This article covers why the general ledger on its own falls short for modern financial institutions, how the subledger offsets underlying product-level complexity and why the subledger is capable of supporting both traditional and forward-looking accounting.

From reporting to steering: Extending the general ledger with a subledger

On its own, the general ledger is too high-level and rigid to handle the complexity, detail and diversity of modern financial instruments, evolving accounting standards and regulatory requirements.

Most general ledger solutions on the market today are designed as cross-industry platforms. They offer generic data models that work well for traditional accounting but cannot fully support financial-industry requirements. To compensate, institutions often inflate the general-ledger coding block with multiple dimensions, from product characteristics, risk attributes and accounting event types to lines of business and regulatory regimes.

For example, a standard journal entry may contain only a few attributes, such as account, cost center and legal entity. But a posting for a financial instrument often requires many more dimensions, such as product type, instrument identifier, risk stage (e.g., IFRS 9), valuation category and accounting event type. A single posting can easily expand from three attributes to twenty or more.

As these dimensions accumulate, the general ledger begins to store vastly more data than it was originally designed for. Posting and reporting processes slow down, reconciliation becomes burdensome and data volumes strain system performance. End-of-day and end-of-month closes take too long, while data models become fragile and operational risks and costs increase.

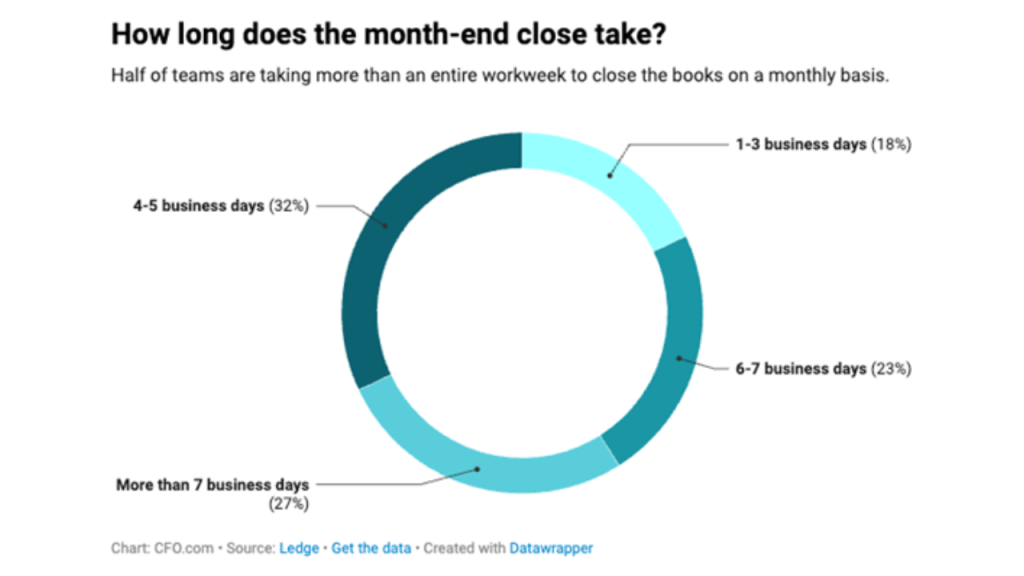

This isn’t theoretical: a finance benchmark cited by CFO.com found cash reconciliation alone often takes 20–50 hours per month, and most teams use 3–5 systems to complete it

This is where the subledger becomes essential.

How a subledger for financial products offsets complexity

Modern subledgers offload detailed product-level accounting, valuation and measurement logic from the general ledger to keep it lean. They handle the complex rules, granular data and event processing that would overwhelm a general ledger, allowing institutions to maintain a clean, efficient and scalable general-ledger environment.

Instead of burdening the general ledger with product-specific calculations, the subledger:

- Captures and validates transaction inputs from multiple systems

- Processes valuation, measurement and risk-based adjustments

- Applies industry-specific accounting rules

- Stores granular accounting documents

- Provides summarized postings that the general ledger can record at the appropriate level of detail

This design keeps the general ledger focused on its true purpose—financial reporting at the aggregated level—while the subledger manages all underlying complexity.

A subledger architecture is particularly critical for banks and insurers operating under IFRS 9, IFRS 17, US GAAP and Solvency II, where accounting calculation logic goes far beyond transactional data. These requirements demand a dedicated accounting engine capable of parallel accounting, data traceability, and multi-regime measurement, all at the most granular level.ine capable of parallel accounting, data traceability and multi-regime measurement, all at the most granular level.

How a subledger supports both expectation-based and traditional accounting

A modern subledger architecture is designed to operate across both accounting worlds:

- Expectation-based accounting, which uses forward-looking data from risk models, such as expected cash flows, expected losses and scenarios.

- Traditional accounting, which uses realized transactions, such as actual payments, drawdowns and interest accruals.

The subledger handles both simultaneously, keeping them loosely coupled. This provides notable benefits, including:

- Flexibility in dealing with events like prepayments

- Reduced manual adjustments

- Lower operational complexity

- Consistent linkage between forecasting and actuals

This is why the subledger becomes essential to US-GAAP and IFRS 9, where expected-loss models must align with accounting outcomes. A general ledger cannot achieve this alignment alone.

1. Subledgers handle modern accounting logic (e.g., IFRS 9 expected cash flows)

OnOne of the clearest examples of accounting that belongs in the subledger, rather than in the general ledger or transactional systems, is the treatment of expected cash flows required under IFRS 9. Modern standards require accounting to reflect forward-looking information such as projected cash flows, expected losses, and behavioral assumptions alongside realized transactions. The subledger is the natural place to incorporate these inputs, apply the appropriate measurement and valuation rules, and produce consistent, auditable accounting results across regimes.

Banks often rely on contractual repayment schedules from their core systems. These schedules are part of the transactional world: they show what the contract says should happen, not what is expected to occur based on customer behavior or macroeconomic conditions.

IFRS 9, however, requires accounting to be based on expected cash flows produced by risk models, which incorporate:

- Expected credit losses

- Prepayment probabilities

- Behavioral repayment patterns

- Macroeconomic scenarios

- Forward-looking adjustments

- Probability-weighted outcomes

This is valuation and risk logic, which the general ledger cannot calculate or store.

The subledger is the natural place for this processing because it uniquely combines:

- Transaction-level granularity

- Multi-regime accounting rules

- Valuation and measurement capabilities

- Risk-integrated data structures

- Auditability and traceability

By centralizing expected-cash-flow accounting in the subledger, institutions ensure correctness, consistency and compliance across risk, finance and reporting.

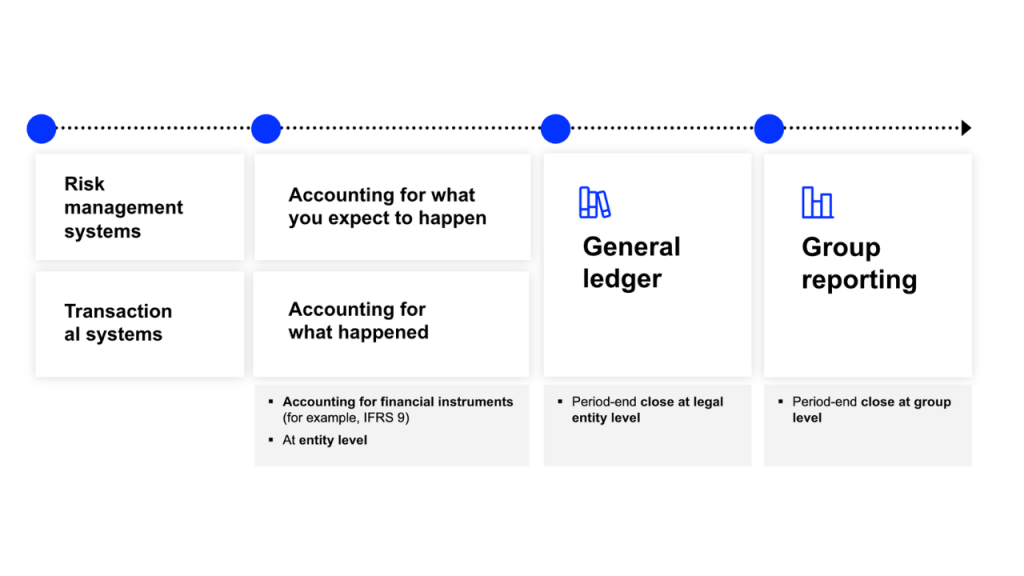

2. The subledger plays a key role in the accounting value chain to ensure transparency

To support both transactional and expectation-based accounting, the subledger should sit at the heart of the accounting value chain. In a modern architecture, the data flow looks like this:

This placement allows the subledger to translate business events (e.g., loan drawdowns, derivative revaluations) into structured accounting documents. The subledger handles the detailed rules, adjustments, and status changes that the general ledger cannot manage efficiently.

It also ensures traceability. Because all data is retained at the most granular level, institutions can track every accounting number back to:

- The originating transaction

- The risk assumptions

- The valuation inputs

- The relevant accounting rule

This level of transparency is essential not only for regulatory compliance but also for internal risk–finance alignment.t.

3. The subledger’s granularity supports consolidation and group reporting

The granularity preserved in the subledger is equally important for producing accurate consolidated results. If coThe granularity preserved in the subledger is equally important for producing accurate consolidated results. If consolidation relies only on the lean, aggregated general ledger, much of the detail required for eliminations, counterparty matching and currency translation disappears.

A well-designed subledger therefore provides consolidation-ready data, enabling:

- Consistent eliminations across entities

- Accurate counterparty identification

- Harmonized currency treatment

- Transparency into intercompany flows

- Traceable adjustments at group level

This creates a consistent foundation for both statutory reporting and internal management reporting.

The subledger provides the foundation for planning, forecasting and decision-making

As the industry evolves, having a consistent source of granular accounting information becomes foundational—not only for external reporting but for business steering.

With a subledger:

- Scenario analysis becomes more accurate

- Planning processes become more reliable

- Finance can integrate risk insights into forecasts

- Decision-makers get a unified view of performance drivers

- Institutions can adapt faster to regulatory and market changes

In this model, the general ledger serves as the clean, stable reporting layer, while the subledger provides the intelligence, detail, and analytical depth that modern finance requires.

Together, the general ledger and subledger form a modern, scalable finance architecture capable of supporting the future of banking and insurance.

Control, confidence and better decisions: Why the right subledger completes the ledger

The general ledger remains the essential system of record for aggregated financial reporting. But as products, standards and regulatory expectations evolve, institutions also need a product subledger that can capture the “why” behind the numbers. It links transactions, valuation movements, and risk assumptions into traceable accounting outcomes.

With the right subledger in place, finance and risk teams maintain control at scale, reduce audit and reconciliation risk through transparent lineage and unlock steering insight that supports faster, better-informed decisions. Together, the general ledger and subledger form a resilient finance architecture built not only to report what happened, but to explain, forecast and manage what happens next.

With deep industry expertise and full SAP integration, SAP Fioneer’s subledger is trusted by banks and insurers navigating transformation, complexity and growth. Contact us to see how a single product delivers the accounting, steering and integration capabilities needed to maintain control, reduce audit risk, and make better decisions.

Related posts

Why a subledger matters in bank and insurer accounting

How FPSL and Financial Control combine to streamline financial close

Most read posts

Unlocking scalable AI in insurance from the core

Rethinking insurance commission complexity as a strategic advantage

What sets modern policy administration systems apart

More posts

Get up to speed with the latest insights and find the information you need to help you succeed.