Why a subledger matters in bank and insurer accounting

6-minute read

Published on: 16 March 2026

Financial institutions’ legacy architectures no longer support the forward-looking, risk-integrated accounting required by modern finance. And despite massive tech investment, many are still constrained by patchwork finance stacks.

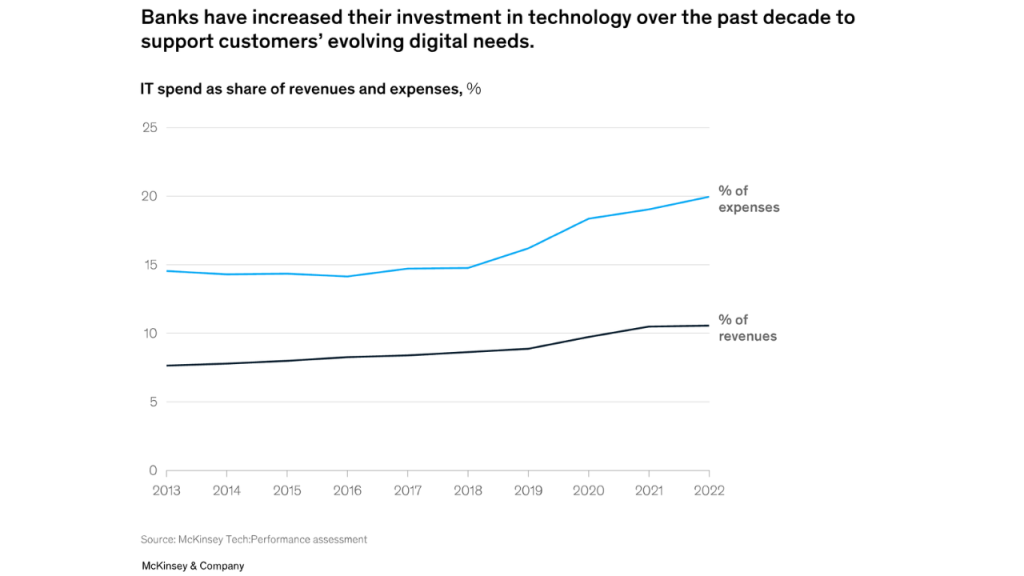

McKinsey estimates banks account for roughly $650B of global annual IT spend, typically 6–12% of revenue, yet value realization is often held back by legacy platforms and fragmented architectures.

Traditional general ledgers, homegrown posting engines and layers of data marts weren’t built for today’s regulatory complexity or ad hoc reporting demands, especially after mergers add even more systems and data models. The result is fragmented data, higher audit risk, rising operational cost and limited ability for finance to steer the business.

In this article, we’ll explain what a subledger is, why it has become essential for modern bank and insurer accounting and what’s driving adoption across the industry.

What a subledger is—and why the general ledger can’t do it alone

A subledger is a detailed accounting layer that sits beneath the general ledger.

Subledgers gained importance when banks and insurers needed to run parallel accounting—local GAAP, US GAAP, IFRS, statutory and regulatory—using a consistent source of data. The general ledger alone could not support multiple measurement bases, or the granular traceability needed for modern regulatory and audit requirements.

With a subledger, however, financial institutions capture all financial product–related events at the most granular level, including operational transactions, valuation adjustments, accruals, risk-driven events and expectation-based calculations. It ensures:

- Full traceability from source system to financial statements

- Automated reconciliation across accounting regimes

- Compliance with increasingly complex standards

- The ability to defend numbers quickly at audit time

This granularity gives finance leaders not only the information needed to meet accounting and compliance demands, but also the ability to drill down into performance drivers for strategic decision-making.

In bank accounting, the subledger serves as a bridge between real-world and contractual (i.e., repayment schedule) transactions and the official accounting books. In insurance, it bridges expectation-based cash flows and statutory/IFRS accounting requirements.

Although bank accounting is increasingly ‘expectation-based’ under IFRS 9, many institutions still use contractual dates as a proxy—something a modern subledger enhances with behavioral and risk-adjusted expectations.

With the introduction of risk capital regimes, such as Basel III/IV and Solvency II, subledgers have also become a critical interface between risk management and accounting, ensuring consistent treatment of credit, liquidity, market and insurance risks. These frameworks elevated the importance of a single source of truth across finance and risk, further increasing the need for unified, granular accounting data.

A unified subledger provides transparency and auditability across products, entities, currencies and reporting regimes. By storing a single repository of granular, persisted data, institutions can run scenarios, generate forecasts and support strategic planning with far greater confidence.

How industry-specific subledger-accounting technology enhances control and decision making

For financial institutions to achieve this level of granularity, control, and analytical capability at scale, industry-specific subledger technology is essential. Modern subledger solutions designed for the financial services industry allow institutions to automate accounting logic, reduce operational effort, and generate strategic insight at accessible cost.

Some subledger technology can even deliver real-time analytics, giving CFOs and CROs visibility into emerging risks, daily profitability drivers and evolving business performance.

Subledgers designed for financial products support the general ledger by:

- Capturing and validating transaction inputs from multiple systems

- Producing clean, compliant accounting entries

- Reflecting both real-world customer activity and contractual repayment schedules

- Supporting expectation-based accounting, now required under IFRS 9/CECL and modern insurance accounting

By consolidating complex, multi-source product data into structured accounting documents and summarized postings, subledgers keep the general ledger lean.

What’s driving subledger adoption in financial institutions?

Financial institutions face simultaneous pressures: regulatory complexity, data fragmentation and the need to modernize finance infrastructure to compete in an AI-enabled industry. These decisions are not marginal. McKinsey estimates that banks spend around $650 billion a year on IT—roughly 6–12% of revenues, the highest share of any major industry—yet many still struggle to realize clear value from this investment due to legacy platforms and fragmented architectures.

These pressures fall into four major categories, each of which contributes to the accelerating adoption of modern subledger systems:

1. Growing regulatory complexity

Standards, such as IFRS and US GAAP, and reporting expectations like Solvency II require:

- Multi-GAAP parallel accounting

- Forward-looking expected loss modeling

- Granular audit trails

- Faster close and submission timelines

- Greater transparency around judgments and assumptions

Compliance now consumes more resources and increases audit risk. The Thomson Reuters’ Cost of Compliance report highlights increasing workloads and resource constraints in compliance teams, while recent UK analysis estimates the annual cost of regulatory compliance for the UK financial services sector at over £33.9 billion.

A subledger helps centralize and automate these requirements while reducing the operational burden of maintaining multiple bespoke processes.

2. Fragmented legacy architectures

Surveys consistently show that legacy technology built around product silos is now one of the biggest obstacles to modernization in financial institutions. Recent research from 10x Banking finds that 55% of banks see their existing core systems as the biggest roadblock to achieving their digital business goals. Other studies reveal that roughly half of financial institutions cite legacy software as a primary barrier to digital transformation and advanced analytics.

These create several issues:

- Data inconsistencies between finance and risk

- Duplicated transformation rules, models and datasets

- Heavy reconciliation workloads

- Reporting delays that hinder decision-making

- Reduced agility in responding to regulatory or business changes

When finance and risk depend on different data sources, consistency and credibility suffer. Management decisions become slower, and regulatory reporting becomes riskier.

A subledger resolves this by serving as a single point of accounting truth, harmonizing data feeds and enforcing uniform rules across products and regions.

3. The push toward digitalization and AI

Institutions are eager to adopt automation, analytics, and AI to reduce manual effort and improve insight generation. Yet AI requires:

- Clean, structured, granular data

- Consistent data definitions

- Transparent audit trails

- Alignment between operational, risk and finance data

Legacy systems cannot provide this because they were never designed to deliver standardized, granular, or consistent data across the organization.

A modern subledger acts as the data foundation for AI adoption, delivering high-quality, standardized inputs that machine-learning tools rely on. This is critical because multiple studies report that the vast majority of AI initiatives fail or underperform due to data problems rather than model limitations. For example, research suggests that around 85% of AI projects fail because of poor data quality or lack of relevant data.

4. Risk of falling behind more agile competitors

Institutions unable to modernize their finance architecture face increasing disadvantages:

- Slower adoption of AI and automation

- Higher cost bases

- Slower decision cycles

- Weaker risk integration

- Reduced ability to support new digital products

Modern competitors like neo-banks, digital insurers and cloud-native lenders operate with cleaner data models and flexible accounting layers, enabling more rapid innovation.

A modern subledger closes that gap, integrating risk, finance and operations into a cohesive accounting and reporting framework for financial institutions.

A modern accounting foundation for control, compliance and scale

As banks and insurers navigate transformation, complexity and growth, the finance architecture has to do more than produce historical statements. A subledger provides the granular, persistent data and parallel-accounting capabilities needed to maintain control across products, entities, currencies and regimes while reducing reconciliation effort and audit exposure.

Just as importantly, it creates a trusted foundation that helps finance and risk operate from the same economic view, improving transparency and decision-making as requirements evolve.

To see how this looks in practice, contact us or book a demo of SAP Fioneer’s subledger.

Related posts

Why expected cash flows are the foundation for risk-integrated accounting

How financial institutions simplify accounting with SAP Fioneer’s subledger

Modernizing finance without losing control: The subledger’s role

Most read posts

What sets modern policy administration systems apart

Unlocking scalable AI in insurance from the core

Rethinking insurance commission complexity as a strategic advantage

More posts

Get up to speed with the latest insights and find the information you need to help you succeed.