Making sense of Use of Proceeds (UoP) structures

Published on: 30 April 2026

With over 600 members, the Partnership for Carbon Accounting Financials (PCAF) standard is widely recognized as the industry benchmark for measuring financed emissions. Many financial institutions have completed initial calculations and are at varying stages of maturity across methodology, data quality and process automation. What began as a reporting exercise is now becoming central to climate risk management and strategic decision-making.

PCAF’s November 2025 update is a major evolution of the standard. It helps financial institutions measure emissions more granularly and comprehensively, strengthens transparency in reporting, and introduces a more forward-looking perspective. That shift supports a move from measurement to active transition management.

At the same time, the update raises expectations. Financial institutions need to keep evolving their practices to meet higher methodological and data requirements. In this blog post, we focus on one of the most important elements of the update: use of proceeds (UoP) structures.

What are Use of Proceeds (UoP) structures?

Use of proceeds structures are financial instruments or arrangements where funds are earmarked for specific projects, assets, or companies (often with a climate or sustainability label). Typical examples include:

- Green or transition bonds issued by corporates, sovereigns, or agencies

- Green or sustainability-linked loans

- Debt or equity funds that invest in defined low-carbon or transition portfolios

- Special purpose vehicles (SPVs) holding a pool of identified assets

Throughout this article, we use the term financed object to describe the project, company, or physical asset that ultimately receives capital and where emissions occur. This helps separate:

- The financial asset on the balance sheet (for example, a bond, loan, or fund unit)

- From the real economy activity (for example, a company, building, or project) that generates emissions

In PCAF terminology, these financed objects are often referred to as “underlying assets”.

What is new in the PCAF UoP methodology?

In standard PCAF asset class methods, there is usually a one-to-one relationship: One exposure leads to one financed object, which leads to one emissions calculation.

UoP structures introduce a more complex one-to-many relationship:

- A single bond, loan, or fund can finance multiple financed objects

- Those objects can span different PCAF asset classes (projects, companies, buildings)

- Some financed objects can themselves be UoP structures, which creates multiple layers of look-through

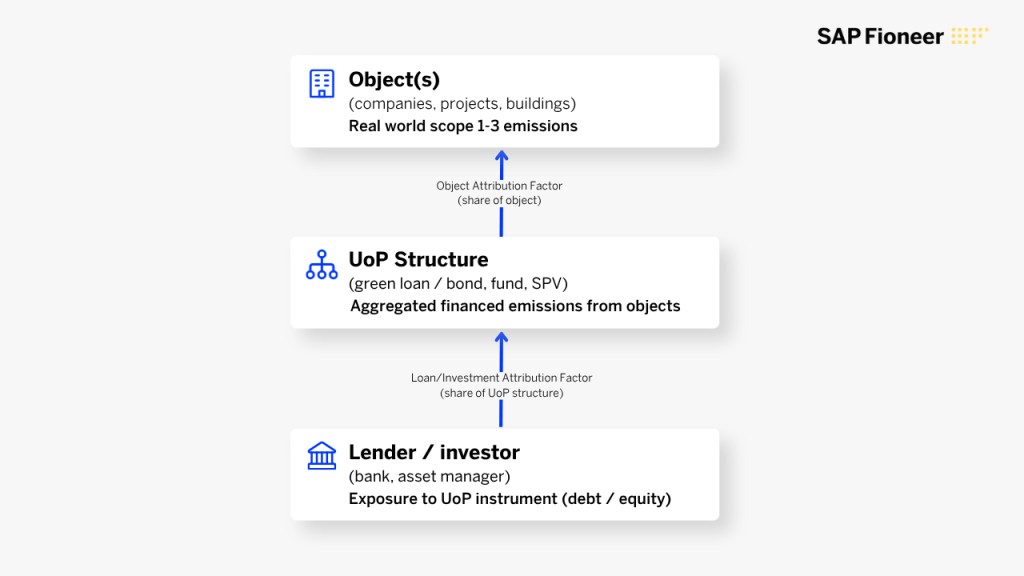

To handle this complexity, PCAF introduces an additional attribution layer at the object level, applied alongside traditional loan-level or investment-level attribution factors.

At a high level, the calculation works as follows:

1. Emissions of the financed objects

For each financed object, reported or estimated emissions are calculated using the relevant PCAF asset class methodology. This is the point where emissions occur.

2. Financed emissions of the UoP structure

An object-level attribution factor is applied to each financed object to determine the share of its emissions financed through the UoP structure. The emissions from all objects are then aggregated to calculate the total financed emissions of the UoP structure.

3. Financed emissions of the lender or investor

Once the UoP structure’s financed emissions are determined, the exposure-level attribution factor is applied to allocate emissions to each lender or investor based on their exposure.

This strengthens the follow-the-money approach, from portfolio exposure, through the UoP structure, down to each financed object’s emissions.

A simple example: one green loan, three projects

Consider a €300 million green loan that finances three projects:

- Wind farm A, total capex (debt + equity): €200mn

- Solar park B, total capex (debt + equity): €150mn

- Grid asset C, total capex (debt + equity): €250mn

The loan is allocated as:

- €100mn to A

- €100mn to B

- €100mn to C

For each project, we compute an object-value attribution factor as:

Outstanding loan amount ÷ total capex

This gives approximate attribution factors of:

- A: €100mn ÷ €200mn = 50%

- B: €100mn ÷ €150mn = 67%

- C: €100mn ÷ €250mn = 40%

Each project’s emissions (calculated using the relevant PCAF category) are then multiplied by its attribution factor. The results are aggregated at UoP structure level and then allocated to the lender or investor based on their exposure.

The outcome is a granular, traceable link between the green loan on the balance sheet and the real economy emissions profile of each underlying project.

From theory to practice: data and system challenges

While the PCAF UoP methodology is conceptually clear, implementing it at scale is not trivial. Financial institutions typically face several challenges:

Data granularity and quality

- Identifying, maintaining and updating financed object data across multiple layers of structures (funds, SPVs, securitizations, labeled bonds)

- Collecting emissions data or proxies for a diverse mix of projects, companies and assets

Look-through and multi-layer attribution

- Applying object-level and exposure-level attribution consistently across nested structures

- Avoiding double counting where the same financed objects appear through different channels

Integration into finance and risk processes

- Aligning financed emissions calculations with existing risk, finance and reporting architectures

- Ensuring results are audit-ready and traceable from portfolio metrics to underlying data points

The methodological requirements for UoP structures are not entirely new. A similar attribution logic has been applied by some institutions in areas such as commercial real estate financing, where a single loan frequently finances multiple buildings. In those cases, the financing facility effectively functions as a UoP structure, with emissions calculated and attributed at the level of each individual building. The updated PCAF guidance formalizes and generalizes this logic across asset classes. It provides a consistent framework for increasingly complex financing structures.

How SAP Fioneer can help

As a PCAF accredited partner for Europe and Central Asia, SAP Fioneer supports financial institutions in adopting the updated standard. With the ESG KPI Engine, SAP Fioneer provides a finance-grade, audit-ready solution that helps institutions configure, calculate, control, and report portfolio-level climate and nature key performance indicators (KPIs), including financed emissions and Net Zero alignment. It is designed to integrate into finance and risk environments, supporting transparency, traceability, and consistent KPI calculation across teams.

If you would like to understand the impact of the PCAF updates, assess your current capabilities, or explore how to operationalize transition management in practice, get in touch with our team to start the conversation.

Most read posts

What sets modern policy administration systems apart

Unlocking scalable AI in insurance from the core

Rethinking insurance commission complexity as a strategic advantage

More posts

Get up to speed with the latest insights and find the information you need to help you succeed.